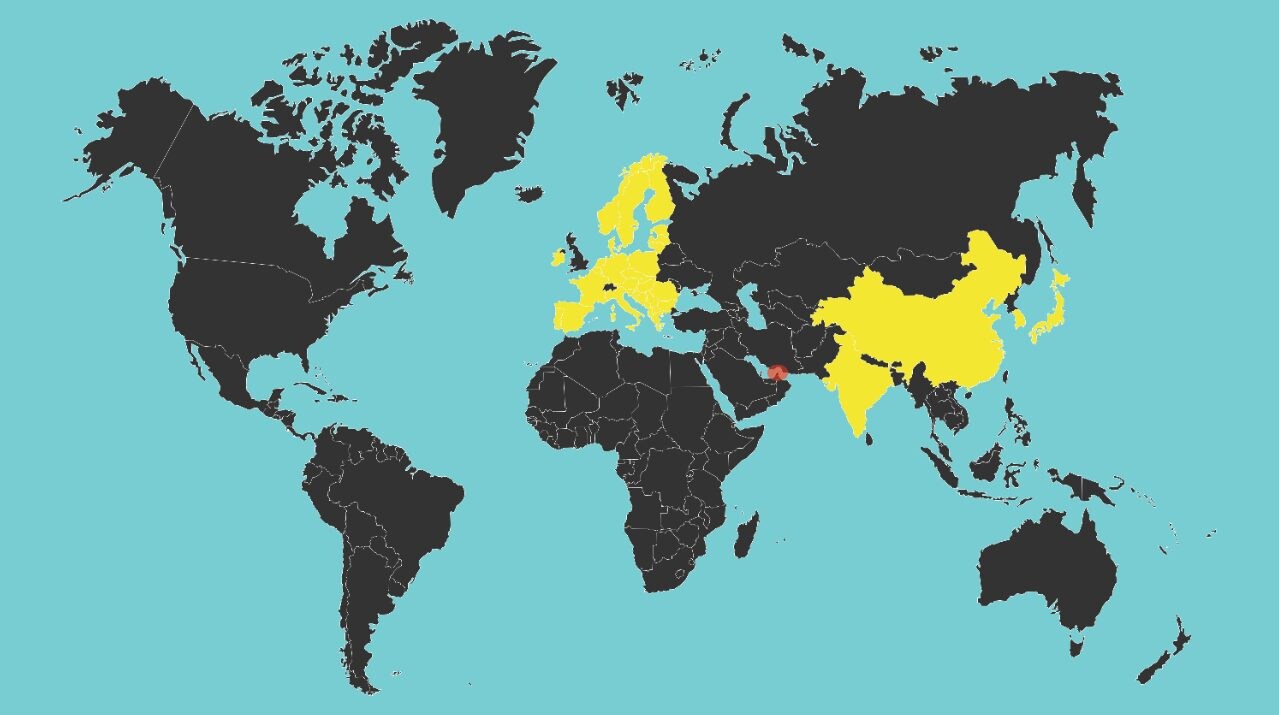

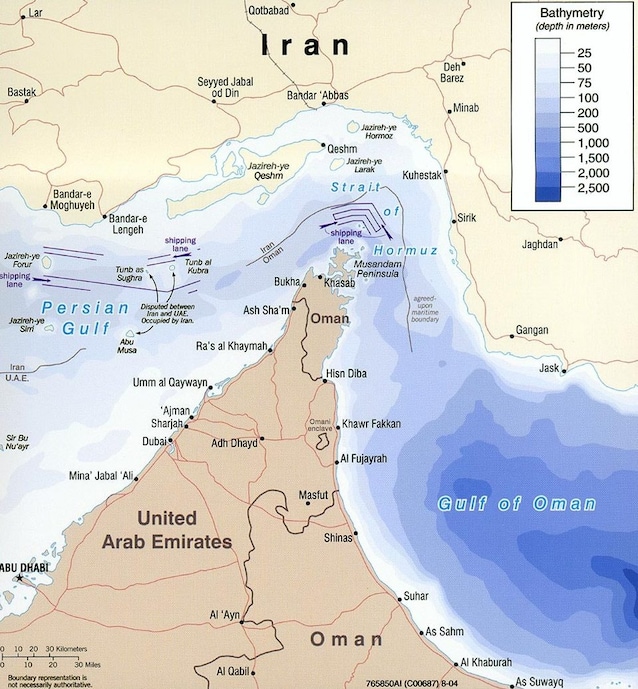

The Strait of Hormuz connect the Persian Gulf al Gulf of Oman and the Indian Oceanwith to the south Oman and to the north Iran. From this sea passage, long 167 km and narrow around 33kmevery day it passes approximately 20% of the world’s oil and of liquefied gas (LNG), with raw material exports coming mainly from Iran, Iraq, Qatar, Kuwait, Saudi Arabia, United Arab Emirates (UAE). The main importers of Iranian oil and gas are Asian countries: mainly China, India, Japan and South Korea. Let’s see in detail what the direct consequences of its closure are on the energy supply of these countries.

Most of the oil and liquefied natural gas (LNG) imported from Middle Eastern countries such as Iran, Iraq, Qatar, Saudi Arabia, Kuwait and the United Arab Emirates (UAE) it doesn’t have alternative sea routes and therefore any crisis or interruption of supplies through this passage has strong repercussions on the markets, mainly Asian. As regards theEuropealthough since 2022 several European countries (mainly France, Germany, Italy, the Netherlands and Belgium) have increased their purchases of LNG since Qatar, the latter have greater diversification in their suppliers, also importing LNG from Africa, United States and Norway. The Strait of Hormuz is crucial both for reasons geographical and economic. From a geographical point of view, it represents the only one natural outlet for almost all the producing countries in the region from the Persian Gulf to the Ocean, as there is no other natural maritime passage that allows it.

Some Gulf countries they tried to find alternative routes but from the point of view of volumes of raw materials the Strait of Hormuz remains crucial: theSaudi Arabia, for example, also uses a pipeline which reaches the port of Yanbu, in the Red Seadiverting part of Saudi exports into this channel. In other cases, such as Qatarthere is no alternative pipeline that can transport LNG without passing through the Strait of Hormuz. In fact, there are neither alternative land pipelines to Asian countries nor liquefaction terminals outside the Gulf; remember that the main one is that of Ras Laffan, managed by QatarEnergy. Just yesterday, following some military drone strikes, the company announced thetemporary interruption of LNG production in Ras Laffan.

In addition to geographical reasons, the construction of new alternative routes to Hormuz would imply theinvestment of tens of billions and the construction of oil pipelines of thousands of kilometres, a less feasible option both in terms of economic resources and timing.

The main cross-Strait exporting countries

THE Countries that use the Strait of Hormuz for oil and LNG exports they are mainly::

- Iran: represents one of the main exporters of crude oil and, although to a lesser extent, gas

- Saudi Arabia: it is the largest oil exporter in the region using this shipping route

- Iraq: together with Iran it represents one of the main exporters of crude oil

- United Arab Emirates: Via the Strait of Hormuz, the UAE exports oil and gas

- Qatar: the country is one of the world’s largest exporters of liquefied natural gas (LNG) which passes through Hormuz, also a supplier to numerous European countries, including Italy

- Kuwait: mainly exports oil across the Strait

The ships they transport LNG and oil tankers who pass through this sea passage head towards the Gulf of Oman, from which they then head towards Asia, Europe and North America, most of which are directed towards China, India, Japan and South Korea.

The main importing countries across the Strait

China

There China is one of the largest importers of oil from Iran through the Strait of Hormuz: it is estimated that approximately 90% of exports Iranian oil companies are headed to the country, passing through theIndian Ocean and arriving in South China Sea. Already in ancient times, the Strait of Hormuz was used for the trade of ceramics, ivory, silk and textiles from China passed through the region. A closure of Hormuz would put a strain on China’s energy security: almost the 30% of its LNG imports come from Qatar and the United Arab Emiratesand about the 40% of its oil imports pass through Hormuzaccording to UBP estimates. Unlike other countries, however, despite being very exposed, the China it has reserves and alternative sources that provide a certain margin of safety. The stocks of LNG of China at the end of February were approximately 7.6 million tonsproviding short-term coverage. However, if the closure of Hormuz and therefore the energy disruption were to continue, the dynamics could intensify price competition throughout Asia. Despite this, China is not the most vulnerable country to potential supply shocks.

India

THE‘India is one of the main ones importers of LNG and crude oilwith ships crossing the Indian Ocean from Hormuz arriving in the Bay of Bengal. At the same time, India, unlike China, is a vulnerable actor in this situation: 60% of India’s oil imports come from the Middle East and more than half of its LNG imports are in fact linked to the Gulf and a significant portion is indexed to Brentone of the main global reference points for determining the price of crude oil. Its price is influenced by the supply and demand of crude oil but also by geopolitical situations, particularly in the Middle East. This means that a spike in crude oil caused by the closure of Hormuz would simultaneously increase i import costs of oil and contract prices LNG.

Japan and South Korea

Japan and South Korea They practically matter all the oil from the Middle East and much of it through the Strait of Hormuz. The route to Japan of ships passing through Hormuz passes through‘Indian Ocean Pacific direction across the Strait of Malacca. According to UBP, the Middle East provides the 75% of Japan’s oil imports and about the 70% of those in South Korea. As for LNG, 14% of LNG of South Korea comes from Qatar and United Arab Emirates, while Japan imports approximately 6%. Economies that have a high dependence on energy imports, such as Japan, South Korea and Taiwan, are therefore more exposed to supply shocks. There South Korea, for example, unlike China, it also has limited reserves and its net oil imports represent the 2.7% of GDPbeing one of the most vulnerable countries in the region in this context.

Europe

To a lesser extent, theEurope is affected by this energy crisis: the route of oil tankers heading to Europe passes through the Cape of Good Hope towards the Atlantic Ocean, then entering the Mediterranean Sea. Compared to Asian countries, however, Europe is less exposed: the LNG, directed to Italy, Belgium, the Netherlands, France and Germany, comes mainly from Qatarwhich provides on average the 10–15% of European LNG. The one that passes through it Strait of Hormuz is about 3-6% of the total gas consumed by the European Union. Due to the diversification of suppliers (United States, Norway, West Africa and Algeria)Europe is therefore less vulnerable to this crisis. As for the raw instead Europe’s dependence is estimated at around 10–15% of importsand therefore direct consequences could be seen mainly in volatility or price increase rather than on physical supplies.